Inflation, Stagflation & Deflation: Real Estate Explained

Hey there! If you’re scrolling through headlines about the economy and wondering how rising (or falling) prices might affect buying your first home, selling a property, or investing in real estate, you’re not alone. Terms like inflation, stagflation, and deflation sound complicated, but they’re actually straightforward once you break them down—like understanding why your weekly grocery bill keeps changing.

In this post, we’ll explain each one in plain English. We’ll cover what causes them, how they shape the broader economy through GDP (the total value of everything produced in the country), jobs, and interest rates, and—most importantly—how they impact the real estate market. By the end, you’ll see why these economic cycles matter for home prices, mortgage rates, and smart buying or selling decisions.

Inflation is when the overall prices of goods and services rise steadily over time. Your dollar simply buys less than it used to. A mild 2% inflation rate per year is normal and healthy for a growing economy. When it climbs higher (say 5-10% or more), that’s when it starts to feel noticeable.

Common causes include:

Market conditions during inflation:

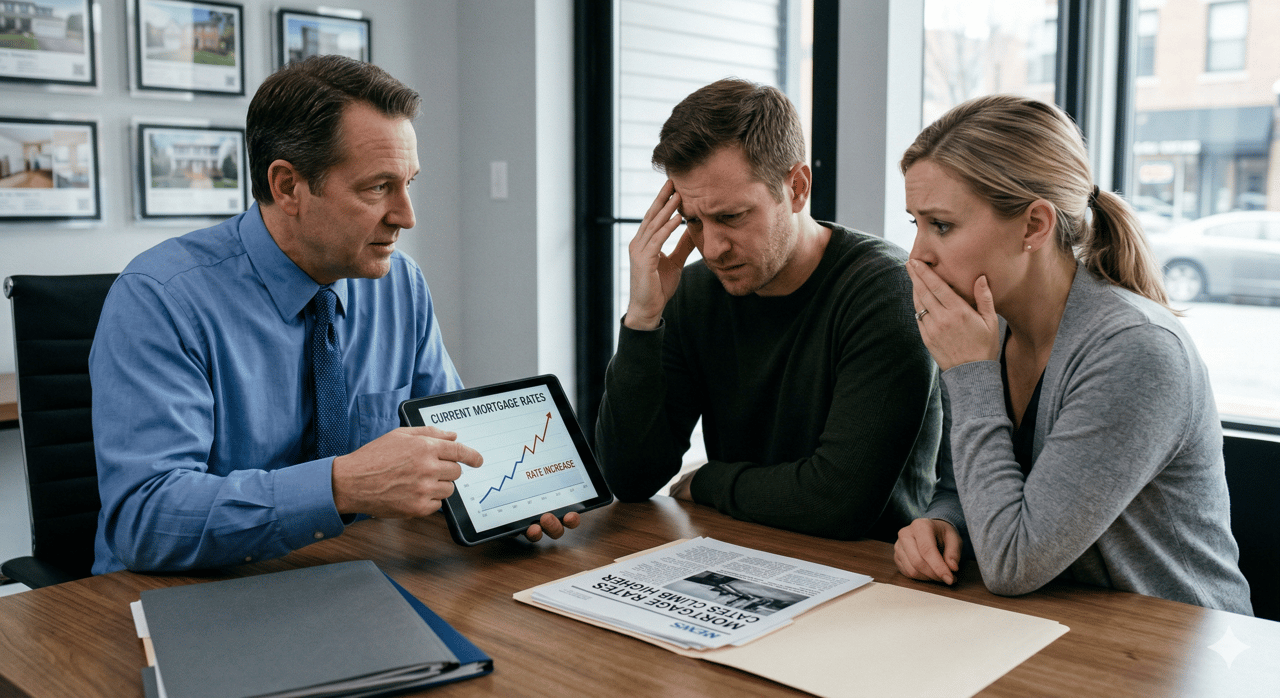

In the real estate world, inflation is often a friend to property owners. Home prices and rents tend to rise right along with (or even faster than) general inflation, making real estate a classic “hedge” against it. If you own a home, its value grows in dollar terms, protecting your wealth. Investors love this because rental income also increases. The downside? Higher interest rates push mortgage rates up, which makes monthly payments more expensive and can slow buyer demand. Fewer people can afford to buy, so the market may see fewer sales even as prices hold steady or keep climbing modestly.

Stagflation is the rare and painful mix of high inflation + stagnant (or shrinking) economic growth + high unemployment. It’s like the economy is stuck in traffic—prices keep rising, but no one is getting ahead.

The classic example is the 1970s U.S. oil crisis: energy prices skyrocketed (a supply shock), pushing up costs everywhere while the economy slowed and jobs disappeared.

What causes stagflation?

Market conditions:

Real estate during stagflation is challenging but not a total disaster. In the 1970s, median U.S. home prices rose about 159% from 1970 to 1982—roughly matching overall inflation—so owners were protected in nominal (dollar) terms. However, real (inflation-adjusted) gains were tiny, and high mortgage rates (which hit 16%+) crushed affordability and sales volume. Buyers sat on the sidelines, new construction slowed, and the market felt frozen even though prices didn’t crash. Today’s investors often view certain real estate segments (especially rental properties or inflation-linked commercial assets) as partial protection because rents can still rise with prices, but expect slower transactions and picky buyers.

Deflation is the opposite of inflation: overall prices fall. At first glance it sounds great (cheaper everything!), but it’s usually a warning sign of serious trouble.

Causes typically include:

Market conditions:

For real estate, deflation is tough. Home prices usually fall because buyers wait for even lower prices and sellers struggle to find them. Mortgage debt stays the same size while your home’s value drops, leaving many “underwater” (owing more than the house is worth). This can lead to more foreclosures and a credit crunch. Lower interest rates help a little by making new mortgages cheaper, but if jobs are scarce and confidence is low, demand stays weak. The Great Depression of the 1930s is the textbook case—home prices plunged nationwide.

| Economic Factor | Inflation | Stagflation | Deflation |

|---|---|---|---|

| Price Direction | Rising | Rising (high) | Falling |

| GDP | Growing | Flat or shrinking | Shrinking |

| Jobs/Unemployment | Low unemployment | High unemployment | Rising unemployment |

| Interest Rates | Rising (to cool economy) | High (policy dilemma) | Falling (to stimulate) |

| Real Estate Prices | Usually rise (good hedge) | Rise nominally but sales slow | Usually fall (painful) |

| Buyer/Seller Impact | Higher rates hurt buyers | High rates + weak jobs = frozen market | Lower rates but weak demand |

No matter which cycle we’re in, real estate remains one of the best long-term ways to build wealth—but timing and strategy matter. In inflationary times, focus on locking in a home before rates climb further. During stagflation, prioritize cash-flow properties or wait for better entry points. In deflationary periods, buyers with strong job security can find bargains, while sellers may need patience or creative financing.

The key takeaway? These economic forces affect home values, mortgage rates, inventory levels, and buyer confidence in very different ways. Understanding them helps you avoid panic-selling at the bottom or overpaying at the top.

At our Reno-based real estate team, we track these trends daily so we can give you clear, practical advice tailored to your goals—whether you’re a first-time buyer, growing family, or investor.

Ready to make your next move with confidence, no matter what the economy throws at us? Reach out today. Ben Florsheim and the team are here to help you navigate any market cycle and turn economic uncertainty into opportunity.

Real Estate

Teething Nights, Turbulent Markets, and What It All Means for You

Whether you're buying, selling, or investing, Ben Florsheim brings deep Reno-Tahoe knowledge and 13+ years of proven success to help you navigate the market with confidence and clarity.