March Newsletter 2026

Things are a little loud at the Florsheim house these days. And I mean that literally. Madison has started teething, which if you’ve been through it, you know what that means: a lot of very long nights, a lot of sympathy cuddles, and more than a few bleary-eyed mornings. She is still somehow the happiest little thing during the day, which makes it all worth it. Erica is doing amazing, a rockstar mom through and through.

Outside of the sleep deprivation, I’ve been heads-down watching what’s shaping up to be one of the more interesting (and honestly unpredictable) real estate markets I’ve seen in a while. There’s a lot happening on the macro side that is filtering its way down to our local Northern Nevada market, and I want to break it all down for you in plain English.

Let me start with the elephant in the room: the conflict in Iran. Whether you’ve been following it closely or just catching headlines, the economic ripple effects are real and they’re hitting the housing market in a very direct way.

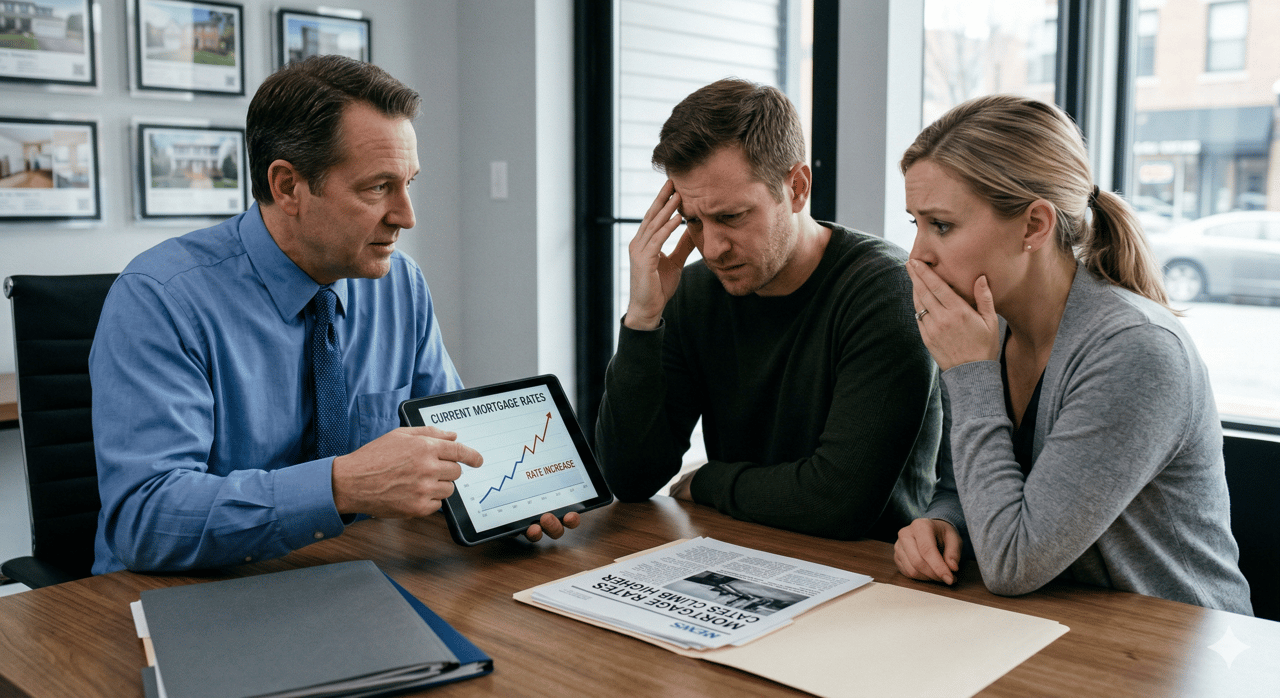

Iran’s effective blockade of the Strait of Hormuz, a critical shipping lane that carries roughly 20% of the world’s oil supply, sent Brent crude oil surging past $119 per barrel. That kind of energy shock is inflationary by nature. When oil gets expensive, everything from transportation to manufacturing to groceries gets more expensive. It reignites the inflation concerns that most of us had hoped were in the rearview mirror.

In the bond market, investors spooked by inflation started demanding higher yields on Treasury notes. The 10-year Treasury yield climbed to around 4.45%, up nearly half a point from 3.96% just before the Iran strikes began. And since mortgage rates closely track the 10-year Treasury, you can guess what happened next. The 30-year fixed mortgage rate jumped from roughly 5.99% to 6.38%–6.5% in just a matter of weeks, rising for four straight weeks to levels not seen in over six months.

Now here’s where it gets interesting, and frankly a little tricky for the Federal Reserve. At their March meeting, the Fed held rates steady at the 3.50%–3.75% range and signaled at most one rate cut for all of 2026. Their core inflation forecast was revised upward to 2.7%. Not what anyone wanted to hear. But at the same time, Chair Powell essentially acknowledged that job creation has slowed to near zero. The labor market, which had been the last pillar of strength in this economy, is starting to show cracks.

My honest take? The Fed is in a genuinely tough spot. Raising rates to fight inflation when the job market is already softening would be counterproductive. It would put more people out of work and potentially tip us into a recession. But holding rates while inflation ticks back up isn’t a great look either. I think they hold steady and hope the energy shock is temporary. Either way, don’t expect significant relief on mortgage rates this year.

Here’s the thing, and I say this to every client right now: macro uncertainty does not mean local paralysis. Northern Nevada still has its own dynamics, and there are real opportunities on both sides of a transaction if you know where to look.

On the seller side, inventory remains tight, which is still putting power in the hands of sellers who price smartly. Homes listed aggressively at or just under true market value are still seeing strong activity. Full-price offers and even over-ask are happening. Buyers haven’t disappeared, they’ve just gotten more discerning. The days of pricing aspirationally and hoping for the best are gone. But if you price right, you can still win big.

New home sales are also shining in this environment. Builders have stepped up in a meaningful way, offering closing cost credits and mortgage rate buy-downs that make a real difference at today’s rates. If you can lock in a buy-down that drops your effective rate a point or more, that’s a significant monthly savings. It’s one of the few areas where buyers are getting genuine relief right now.

On the buyer side, deals are absolutely out there. You just have to know where to find them. The best opportunities right now are in two places: listings that have been sitting on the market for an extended period, and homes that need some work. Extended days on market almost always signal pricing that got ahead of itself. Sellers in those situations are often much more motivated, and I’m seeing successful negotiations that include reductions in purchase price, closing cost credits, and repair concessions negotiated in escrow. Sometimes all three.

The bottom line is this: the market rewards preparation and decisiveness. Buyers who are pre-approved, know their numbers, and are ready to move have the advantage. Sellers who trust the data and price accordingly are still winning. The noise from the macro environment is real, but it doesn’t have to sideline you.

As always, if any of this sparks questions about your own situation, whether you’re thinking about buying, selling, or just curious about where things stand, please reach out. I love talking through the market and helping people make smart, confident decisions. Hit reply, give me a call, or let’s grab a coffee.

And if you know a great nanny, seriously, send them my way. 😄

Wishing you a wonderful spring ahead,

Whether you're buying, selling, or investing, Ben Florsheim brings deep Reno-Tahoe knowledge and 13+ years of proven success to help you navigate the market with confidence and clarity.